Practicing the CUET Accountancy question paper with answers is essential for sharpening your conceptual clarity and building exam-day confidence. Download your free CUET UG Accountancy 2026 practice paper PDF and start prepping to secure a top score.

The CUET UG 2026 entrance exam is currently underway, and candidates are actively searching for previous years' papers and model sets to understand the latest question patterns and difficulty levels. As a gateway to top-tier undergraduate programs like B.Com (Hons), the CUET Accountancy section requires rigorous practice in these final stages. To help you excel, we have compiled a high-yield collection of important CUET Accountancy questions and detailed solutions right here.

CUET Accountancy Question Paper 2026

The CUET Accountancy paper is a computer-based test (CBT) with a 60-minute duration, featuring 60 objective-type multiple-choice questions (MCQs). Success depends on mastering the question patterns from 2026 and previous years. Our in-house experts have developed a memory-based practice paper grounded in real-time student reviews, which is vital for those appearing in upcoming shifts. Make sure to thoroughly review the CUET Accountancy exam syllabus to maximize your potential for a high score.

CUET Accounts Question Paper 2025 PDF Download

Download the official CUET Accountancy practice paper with complete solutions in PDF format from the table provided below.

| Shifts | CUET Accounts Question Paper PDF link |

| CUET Accounts Question Paper 2025 (May 13 Shift 1) | Download PDF |

| CUET Accounts Question Paper 2025 (May 13 Shift 2) | Download PDF |

| CUET Accounts Question Paper 2025 (May 14 Shift 2) | Download PDF |

CUET Accountancy Important Questions with Answers

The expert faculty at Result91 has curated the top 100+ most important questions for the Accountancy subject. Each question is accompanied by an in-depth solution to clarify complex concepts. These materials have been rigorously compiled based on extensive research of previous years' exam trends and core syllabus requirements.

Our content team has analyzed the latest NTA question paper trends to identify the 100 most anticipated questions that are likely to appear in the current CUET UG Accountancy exam. By practicing these high-probability questions, candidates can significantly boost their preparation and improve their final rank.

CUET Accountancy Question Paper Pattern 2026

The NTA has updated the CUET Accountancy exam pattern for 2026, removing internal options; students are now required to attempt all questions. While the structure of the exam pattern has shifted, the NTA has maintained the existing marking scheme for the 2026 cycle.

| CUET Accountancy Exam Pattern 2026 | |

|

Exam Parameters |

Exam Details |

|

Examination Mode |

Computer-Based Test (Online) |

|

Question Type |

Multiple Choice Questions (MCQs) |

|

Total Question Count |

50 questions |

|

Negative Marking |

Yes |

|

Marking Scheme |

+5 per correct answer -1 per incorrect answer |

|

Exam Language Medium |

13 languages: English, Hindi, Assamese, Bengali, Gujarati, Kannada, Malayalam, Marathi, Odia, Punjabi, Tamil, Telugu, and Urdu. |

View Detailed CUET Syllabus 2026

CUET Accounts Important 100 Questions with Answers

Q1. Rearrange the items under the "Equity and Liabilities" head of the Balance Sheet according to the Companies Act 2013, Schedule III.

(A) Current Liabilities

(B) Shareholders’ funds

(C) Share application money pending allotment

(D) Non-Current Liabilities

Select the correct sequence from the options below:

(a) (B), (C), (D), (A)

(b) (C), (B), (A), (D)

(c) (A), (B), (C), (D)

(d) (D), (C), (A), (B)

Q2. Match List – I with List – II.

| List – I | List – II |

| (A) MS Access | (I) Horizontal row of the table |

| (B) DBMS | (II) Vertical column of the table |

| (C) Field | (III) Data Base management software |

| (D) Record | (IV) Data Base management system |

Choose the correct answer from the options provided:

(a) (A)-(II), (B)-(IV), (C)-(III), (D)-(I)

(b) (A)-(IV), (B)-(III), (C)-(II), (D)-(I)

(c) (A)-(III), (B)-(IV), (C)-(II), (D)-(I)

(d) (A)-(IV), (B)-(III), (C)-(I), (D)-(II)

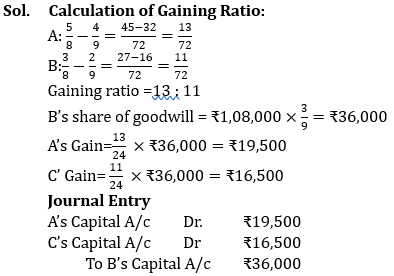

Q3. A, B, and C are partners sharing profits in a ratio of 4:3:2. Upon B's retirement, goodwill is valued at ₹1,08,000. If A and C decide to share future profits in a 5:3 ratio, what is the necessary journal entry?

Journal Entry Options:

(a) A’s capital A/c Dr ₹18,000

C’s capital A/c Dr ₹18,000

To B’s capital A/c ₹36,000

(b) A’s capital A/c Dr ₹67,500

B’s capital A/c Dr ₹40,500

To C’s capital A/c ₹1,08,000

(c) B’s capital A/c Dr ₹36,000

To A’s capital A/c ₹19,500

To C’s capital A/c ₹16,500

(d) A’s capital A/c Dr ₹19,500

C’s capital A/c Dr ₹16,500

To B’s capital A/c ₹36,000

To C’s capital A/c ₹16,500

Q4. Avtar Ltd. issued 80,000 shares at ₹10 each (₹5 application, ₹3 allotment, ₹2 call). Applications were received for 2,50,000 shares. After rejecting 30,000 shares and allotting the rest on a pro-rata basis, determine the refund amount at the time of allotment.

(a) ₹1,50,000

(b) ₹6,10,000

(c) ₹4,60,000

(d) ₹4,50,000

Q5. Which of the following facts pertain to the dissolution of a partnership firm?

(A) The firm's business is closed.

(B) Assets are sold, and liabilities are discharged.

(C) A firm can be dissolved by court order.

(D) Books of account are closed.

(E) Economic relationships between partners continue in a modified form.

Select the correct option:

(a) (A), (B), (C), and (D) only

(b) (A), (B), (C), and (E) only

(c) (A), (B), (D), and (E) only

(d) (A), (B), (D), and (C) only

Q6. Securities Premium Reserve can be legally utilized for which of these purposes?

(A) Issuing fully paid bonus shares

(B) Writing off preliminary expenses

(C) Paying premiums on redemption of preference shares or debentures

(D) Distributing dividends to shareholders

(E) Writing off company losses

Select the correct option:

(a) (A), (B), and (E) only

(b) (A), (B), and (D) only

(c) (A), (B), and (C) only

(d) (C), (D), and (E) only

Access CUET Previous Year Question Papers

Q7. Which financial statement analysis tool evaluates the relationship between two accounting figures?

(a) Comparative statement

(b) Common size statement

(c) Ratio Analysis

(d) Cash flow statement

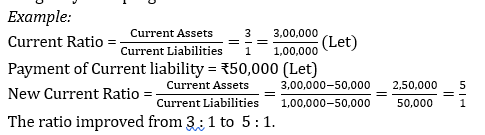

Q8. A firm has a current ratio of 3:1. What is the impact of paying off a current liability on this ratio?

(a) Improves the current ratio

(b) Reduces the current ratio

(c) No change in current ratio

(d) Affects the solvency ratio

Q9. In the absence of a partnership deed, what rules apply?

(A) Partners get interest on capital at 6% p.a.

(B) Partners get interest on loans at 6% p.a.

(C) Partners receive salary for active participation.

(D) Profits are shared in the capital ratio.

(E) Profits are shared equally.

Select the correct option:

(a) (A) and (C) only

(b) (B) and (C) only

(c) (B) and (E) only

(d) (C) and (D) only

Q10. Which of the following statements relate to the Income and Expenditure A/c?

(A) Includes opening and closing cash balances.

(B) Prepared on an accrual basis.

(C) Records revenue-nature expenditures only.

(D) Records both revenue and capital expenditures.

(E) Includes non-cash transactions like depreciation.

Select the correct option:

(a) (A), (D), and (E) only

(b) (B), (C), (D), and (E) only

(c) (B), (C), and (E) only

(d) (C), (D), and (E) only

Q11. Which facts relate to Cash Flows from Operating and Investing Activities?

(A) Interest/dividend receipts are operating inflows.

(B) Royalty/fee receipts are operating inflows.

(C) Employee benefit payments are operating outflows.

(D) Plant purchase payments are investing outflows.

(E) Tax payments are financing outflows.

Select the correct option:

(a) (A), (B), and (C) only

(b) (B), (C), and (D) only

(c) (C), (D), and (E) only

(d) (A), (B), and (E) only

Q12. Calculate the Cash Flow from Financing Activities based on the provided company data.

April 1, 2016 to March 31, 2017 comparison data.

Currency in (₹)

Long term loans: 2,00,000 (2016) to 2,50,000 (2017)

Loan repayment during the year: ₹1,00,000

(a) Outflow ₹50,000

(b) Inflow ₹1,50,000

(c) Outflow ₹1,50,000

(d) Inflow ₹50,000

Q13. Match List – I with List – II.

| List – I | List – II | ||

| (A) | In accordance with a contract between the partners | (I) | Compulsory dissolution |

| (B) | When business becomes illegal | (II) | Dissolution by court |

| (C) | Death of partner | (III) | Dissolution by agreement |

| (D) | Partner became insane | (IV) | Happening of certain contingencies |

Select the correct option:

(a) (A)-(III), (B)-(I), (C)-(IV), (D)-(II)

(b) (A)-(I), (B)-(III), (C)-(IV), (D)-(II)

(c) (A)-(III), (B)-(I), (C)-(II), (D)-(IV)

(d) (A)-(I), (B)-(III), (C)-(II), (D)-(IV)

Q14. If Securities Premium Reserve is insufficient, from which account is the loss on issue of debentures written off?

(a) Debenture Redemption Reserve

(b) Statement of Profit and Loss

(c) Premium on redemption of Debentures A/c

(d) Reserves and Surplus

Q15. What are the steps to prepare an Income and Expenditure account?

(A) Assign revenue receipts/expenses to the appropriate account side.

(B) Review the Receipt and Payment Account.

(C) Exclude all capital items.

(D) Close the account to determine surplus or deficit.

Select the correct option:

(a) (D), (C), (B), (A)

(b) (B), (C), (A), (D)

(c) (C), (B), (A), (D)

(d) (A), (B), (C), (D)

Q16. Upon admission of a partner, how is the reduction in asset value recorded?

(a) Cash A/c

(b) Partner’s Capital A/c

(c) Realisation A/c

(d) Revaluation A/c

Q17. If a creditor accepts an asset valued higher than the liability due to them, how is it handled?

- He will pay excess amount

- He will not pay anything

- The excess amount will be credited to Realisation Account

- The excess amount is debited to Realisation account

- The excess amount is debited to Bank account

Select the correct option:

(a) A, C, and E only

(b) A, B, and C only

(c) B, C, and D only

(d) C, D, and E only

Q18. According to the Companies Act 2013, which disclosures related to share capital are mandatory for the 5 years preceding the balance sheet date?

- Number and class of shares bought back

- Shares reserved under contracts/ commitments

- Forfeited shares

- Number and class of shares allotted for consideration other than cash and bonus shares

- Calls unpaid (Aggregate)

(a) A, B, and C only

(b) B, C, and D only

(c) A, B, and D only

(d) C, D, and E only

Q19. Identify the correct sequence for the statement of profit or loss.

- Other Income

- Total Expenses

- Revenue from Operations

- Profit before extraordinary items & tax

- Total Revenue

Select the correct option:

(a) C, D, A, B, E

(b) C, D, E, A, B

(c) C, A, E, B, D

(d) A, B, C, D, E

Q20. If partners A and B (ratio 3:2) admit Z, and he receives an equal share (1/16) from each, calculate the sacrificing ratio of A and B.

(a) 3:2

(b) 1:1

(c) 43:27

(d) 2:1

Solutions

S1. Ans. (a)

Sol. The correct order for items of "Equity and Liabilities" per the Companies Act 2013 is as follows:

(B) Shareholders’ funds: Includes equity/preference share capital, reserves, and surplus.

(C) Share application money pending allotment: Funds received for shares yet to be allocated.

(D) Non-Current Liabilities: Long-term obligations like loans, debentures, and long-term borrowings.

(A) Current Liabilities: Short-term obligations payable within one year (e.g., trade payables, accrued expenses).

S2. Ans. (c)

Sol. (A) MS Access – (III) Database management software: Software used for creating and managing databases.

(B) DBMS – (IV) Database management system: A software system facilitating database management.

(C) Field – (II) Vertical column of the table: Represents individual data elements in a table.

(D) Record – (I) Horizontal row of the table: Represents collections of related data elements.

S3. Ans. (d)

Sol.

S4. Ans. (c)

Sol.

S5. Ans. (a)

(A) Business is closed: Dissolution marks the cessation of firm operations.

(B) Assets sold/liabilities paid: Assets are liquidated to settle obligations.

(C) Court order: Courts may mandate dissolution for protection or during disputes.

(D) Account books closed: Finalizing financial records and settling all transactions.

S6. Ans. (c)

Sol. Securities Premium Reserve can be used for five specific purposes:

(a) Issue fully paid bonus shares.

(b) Write off preliminary expenses.

(c) Write off issue-related expenses, commissions, or discounts on securities.

(d) Pay premium on redemption of preference shares or debentures.

(e) Buy-back of company shares.

S7. Ans. (c)

Sol. Ratio analysis helps evaluate financial performance, liquidity, and profitability by comparing accounting line items.

S8. Ans. (a)

Sol. A 3:1 current ratio improves when current liabilities are settled with current assets.

S9. Ans. (c)

Sol. Key provisions for partnership accounting in the absence of a deed:

(a) Profits: Shared equally.

(b) Interest on Capital: Not entitled unless agreed.

(c) Interest on Drawings: Not charged.

(d) Interest on Loan: Fixed at 6% p.a.

(e) Remuneration: Not allowed.

S10. Ans. (c)

Sol. Statements relevant to the Income and Expenditure Account:

(B) Accrual basis: Revenue earned and expenses incurred are recognized accordingly.

(C) Revenue-nature: Primarily for recurring operational items.

(E) Non-cash transactions: Includes items like depreciation.

S11. Ans. (b)

Sol. Correct classification of Cash Flows:

(B) Royalty/fee receipts: Operating inflows.

(C) Employee benefit payments: Operating outflows.

(D) Plant purchase: Investing outflow.

S12. Ans. (d)

Sol.

Cash Flows from Financing Activities Analysis

| Particulars | ₹ |

| Loan Acquired | 1,50,000 |

| Loan repaid | (1,00,000) |

| Cash generated from Investing activities | 50,000 |

Working Note:

Long term Loans Account

| Particulars | ₹ | Particulars | ₹ |

| To Bank | 1,00,000 | By Balance b/d | 2,00,000 |

| To Balance c/d | 2,50,000 | By Bank (Bal. fig – Loan acquired) | 1,50,000 |

| Total | 3,50,000 | Total | 3,50,000 |

S13. Ans. (a)

Sol. (A) Contract between partners: Voluntary dissolution.

Agreement-based termination.

(B) Illegal business: Compulsory dissolution.

(C) Partner death: Contingency-based dissolution.

(D) Insanity: May lead to dissolution via court order.

S14. Ans. (b)

Sol. If the Securities Premium Reserve is exhausted, losses on debentures are charged to the Statement of Profit and Loss.

S15. Ans. (b)

Sol. Proper steps for preparing Income and Expenditure A/c:

(B) Peruse Receipt and Payment: Identify all transactions.

(C) Exclude capital items: Separate capital from revenue.

(A) Record revenue items: Credit receipts/Debit expenses.

(D) Determine balance: Calculate surplus or deficit.

S16. Ans. (d)

Sol. Reductions in asset value are debited to the Revaluation Account to accurately adjust valuation upon admission.

S17. Ans. (a)

Sol.

- He will pay excess amount: The creditor will pay the excess amount because the asset provided is worth more than the debt owed to them.

- The excess amount will be credited to Realisation Account: The excess amount is added to the Realisation Account to record it as an asset realized during the dissolution of a partnership.

- The excess amount is debited to Bank account: Simultaneously, the excess amount is debited to the Bank account because it represents an inflow of cash or a valuable asset into the firm’s bank account.

S18. Ans. (c)

Sol. Disclosures regarding share capital required by the Companies Act 2013.

- Number and class of shares bought back: Companies must disclose the details of shares they repurchased during the specified 5-year period.

- Shares reserved under contracts/commitments: This disclosure informs stakeholders about shares set aside for future issuance as per contracts or commitments.

- Number and class of shares allotted for consideration other than cash and bonus shares: Companies need to disclose shares issued in exchange for non-cash consideration and bonus shares issued during the specified 5-year period.

S19. Ans. (c)

Sol. Correct logical sequence for the profit or loss statement.

- Revenue from Operations: This is the starting point, as it represents the primary source of income generated by the company.

- Other Income: After accounting for revenue from operations, other income is added. Other income includes non-operational income sources, such as interest, rent, or dividends.

- Total Revenue: This is the sum of revenue from operations and other income, representing the company’s total income for the period.

- Total Expenses: Next, total expenses are subtracted from the total revenue. This includes all the costs and expenditures incurred by the company in the relevant period.

- Profit before Extraordinary Items & Tax: Finally, after subtracting total expenses from total revenue, you arrive at the profit before considering extraordinary items and tax. This represents the company’s operating profit.

S20. Ans. (b)

Sol. Since both A and B sacrifice an equal share (1/16) for Z, their sacrificing ratio is 1:1.

Additional practice questions and solutions are provided in the PDF below.

Sharing is caring!

FAQs

Candidates have exactly 60 minutes to complete the CUET UG Accountancy exam.